Managing payroll across multiple countries creates significant challenges for growing businesses. Different tax regulations, varying labor laws, fluctuating exchange rates, and diverse compliance requirements transform straightforward compensation into a complex operational puzzle. Companies need reliable solutions to streamline global payments while ensuring compliance across all jurisdictions. The right platform can eliminate manual processes and reduce the administrative burden of managing international teams.

Modern businesses require unified systems that handle multi-country payroll processing, tax calculations, and compliance requirements from a single dashboard. Rather than juggling multiple vendors or managing spreadsheets across time zones, companies can leverage comprehensive platforms that manage contractor payments, employee salaries, and benefits administration for global workforces. Organizations seeking to simplify their international compensation processes should explore robust payroll software designed specifically for global operations.

Table of Contents

- Getting Paid Globally Is Still Harder Than It Should Be

- What “International Payroll Software” Actually Means for Workers

- Why Most Platforms Still Fall Short for Global Workers

- 10 Best International Payroll Software for Global Workers

- How to Choose the Right Platform as a Freelancer or Digital Nomad

- How Ontop Helps You Get Paid Faster and Keep More of It

- Book a Demo Today - See why 950+ Companies Trust OnTop to Power their Global Teams

Summary

- According to industry data, cross-border payment fees typically range from 3-7% of the transaction value, meaning workers can lose $60 to $140 on a $2,000 payment to fees and unfavorable exchange rates. This isn't a processing charge; it's a direct reduction in negotiated compensation that compounds monthly for anyone working internationally. The gap between what clients pay and what workers receive often stays hidden until funds have already moved through intermediary banks and currency conversion spreads.

- Payment timing creates real cash-flow problems beyond mere inconvenience. Traditional international transfers take three to five business days when routed through correspondent banking networks, forcing workers to cover immediate expenses on credit or savings while waiting for funds to clear. A three-day delay during currency fluctuation can cost an additional 2-3% of a paycheck before it reaches the account, turning payment infrastructure into a financial liability rather than a simple transaction.

- Most international payroll platforms were designed to address employer compliance issues, not workers' financial needs. Companies choose systems based on reporting dashboards and bulk processing capabilities, while the worker experience becomes an afterthought. This creates a system where payments arrive, but workers still face currency exposure, withdrawal limitations, and fees that weren't disclosed during contract negotiations, with no tools to manage income across multiple countries and currencies.

- Modern payment infrastructure can complete global payroll processing in as little as 30 minutes compared to the four hours required by manual processes, yet many platforms still route funds through decades-old correspondent banking networks. The modern interface doesn't change the fact that money travels through systems designed when fax machines were cutting-edge technology, which explains why "instant" platform payments still take days to reach local accounts.

- Workers operating globally need more than deposit confirmations. They need accounts that function across borders, spending tools that don't penalize international use, and the ability to hold funds in stable currencies when local inflation erodes value daily. Platforms that end involvement at payout, with no multi-currency wallet or international debit card, fail to address the financial reality of managing income originating in multiple countries.

- Payroll software addresses this by treating cross-border payments as the default rather than the exception, handling compliance, tax calculations, and currency conversion transparently while providing workers with global accounts and spending tools that function across borders.

Getting Paid Globally Is Still Harder Than It Should Be

The systems that move money across borders were designed for banks and corporations, not for global workers. While remote work has become borderless, payment systems remain trapped in a framework built around physical branches, correspondent banking relationships, and currency controls that treat every cross-border transaction as an exception rather than the norm.

🎯 Key Point: Traditional banking infrastructure creates unnecessary friction for remote workers who need seamless global payments as part of their daily workflow.

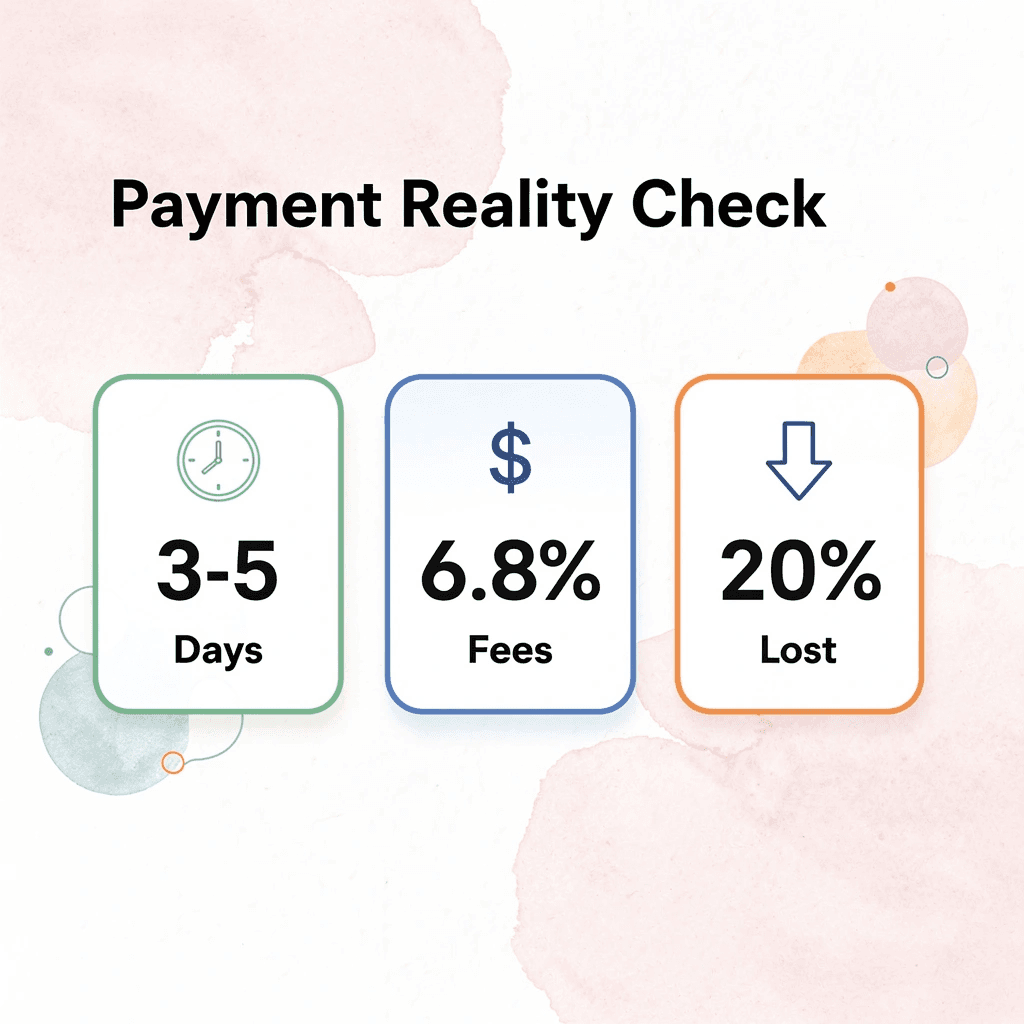

"Cross-border payments still take 3-5 business days on average and cost 6.8% in fees globally, making them one of the most inefficient financial processes in the modern economy." — World Bank, 2023

⚠️ Warning: Many freelancers and remote workers lose 15-20% of their earnings to payment delays, currency conversion fees, and banking charges that weren't designed for the modern global workforce.

What real challenges do global workers face with payments?

This creates real friction. A freelancer in Argentina invoicing a client in Germany watches money move through intermediary banks, lose value to exchange rate margins she never agreed to, and arrive days later than promised. The delay creates cash flow uncertainty that disrupts rent payments, bill schedules, and expense planning.

What are the typical cross-border payment fees?

According to HRZone, cross-border payment fees range from 3% to 7% of the transaction value. On a $2,000 payment, that's $60-$140 lost to fees and unfavorable exchange rates, reducing actual compensation below negotiated amounts. For workers depending on a consistent income, this gap compounds monthly.

How do payment delays affect international workers?

Payment delays compound the problem. Freelance work often pays better per hour than regular jobs, but extra steps and paperwork erode that advantage. One person with multiple languages and a Master's degree earned 3,000 RMB for two days of remote work compared to a 7,500 RMB monthly salary. The higher hourly rate was clear, yet visa rules, payment platforms, and currency conversion created enough friction to make it feel riskier than steady employment.

When payment systems don't match work reality

Young professionals entering the global workforce face structural barriers unrelated to their skills. A 16-year-old freelancer can deliver professional-quality work to international clients but cannot legally sign contracts or access many payment platforms. Age restrictions, platform commissions taking 20% of earnings, and the inability to navigate international tax obligations without formal legal standing create a system in which capability doesn't translate into fair compensation.

How do modern platforms solve cross-border payment challenges?

Platforms like Ontop normalize cross-border payments by routing them through global accounts designed for international work, rather than through multiple intermediary banks that charge unpredictable fees and delays. The system handles compliance, tax calculation, and currency conversion transparently, eliminating extra work.

What's the real barrier to accessible global payments?

The real issue isn't that global payments are impossible—it's that existing systems weren't built with them in mind, and the gap between what's technically possible and what's available remains wider than it needs to be. Understanding the infrastructure problem matters less than how it affects the people who depend on it.

Related Reading

- Pay International Employees

- How Much Does It Cost To Outsource Payroll

- Global Payroll Implementation

- Benefits Of Hiring Remote Workers

- International Payroll Management

- Multi-Country Payroll Outsourcing

What “International Payroll Software” Actually Means for Workers

International payroll software isn't background infrastructure—it controls when your rent gets paid, how much of your invoice you keep, and whether you're protected if something goes wrong. The platform your employer or client uses determines your financial stability.

🎯 Key Point: The payroll platform your company chooses has a direct impact on your day-to-day finances—from payment timing to tax compliance and currency conversion rates.

"International payroll software directly controls the financial stability of remote workers by managing payment timing, tax compliance, and currency conversions." — Financial Technology Research, 2024

💡 Tip: Always ask your employer about their payroll platform's features before starting work—understanding payment schedules, currency options, and support availability can prevent costly surprises down the road.

Speed decides cash flow, not just convenience

When you get paid, it matters in real life. If money takes five days to arrive, you must use a credit card or savings to pay bills. Modern systems can deliver funds in 24 hours or less by eliminating correspondent banking steps. This isn't about convenience—it's about paying your phone bill on time or explaining to your landlord why an international transfer hasn't arrived.

Why do currency fluctuations make speed even more critical?

Workers in countries with fluctuating currency values face significant losses due to payment delays. A three-day delay during exchange rate fluctuation can cost 2-3% of your paycheck before it reaches your account. On a $3,000 monthly payment, that's $60 to $90 lost to processing delays.

Fees aren't always visible until after the fact

You agree to a rate, invoice the amount, then discover the final deposit is smaller than expected. Currency conversion spreads, intermediary bank charges, and platform fees accumulate silently. According to Safeguard Global, international payroll compliance requires navigating different tax codes, labor laws, and reporting standards across jurisdictions, though many platforms conceal these costs until funds have moved.

The best systems show you the breakdown upfront: total fees, exchange rate applied, and expected arrival amount. Transparency lets you plan accurately instead of adjusting your budget after each payment.

Legal protection runs through the same infrastructure

Without proper contracts and compliance structures, you're exposed to client disputes, payment issues, and misclassification risks in foreign legal systems. Platforms like Ontop handle contractor agreements, tax calculations, and compliance automatically, establishing the legal framework before problems arise. You avoid chasing documentation or hiring lawyers to interpret labor laws in unfamiliar jurisdictions.

What risks do cross-border workers face without proper software?

Misclassification risks, unclear contract terms, and payment disputes occur frequently in cross-border work. The software either anticipates these issues or leaves you to solve them after they've damaged your income and working relationship. But even when payments arrive on time and fees stay reasonable, most platforms treat workers as endpoints rather than people managing financial lives across multiple countries.

Why Most Platforms Still Fall Short for Global Workers

The company that pays you chose the platform based on what they needed, not what you needed. They optimized for compliance dashboards, bulk processing, and accounting integrations. Your experience was an afterthought in the vendor pitch deck.

🎯 Key Point: Most payment platforms prioritize employer convenience over worker experience, leaving global talent to navigate complex financial challenges alone.

The payment arrives, but the infrastructure stops there. You're left to manage currency exposure, navigate withdrawal limitations, and absorb undisclosed fees. The platform solved the employer's problem. Yours is beginning.

"Payment platforms are designed for employers first, workers second. The result? Global talent bears the hidden costs of poorly designed financial infrastructure." — Global Workforce Report, 2024

⚠️ Warning: What looks like a simple payment solution to your employer often becomes a complex financial burden for you as the recipient.

- Employer priority

- Compliance dashboards

- Currency exposure risk management

- Bulk processing efficiency

- Accounting integrations

- Worker reality

- Limited visibility into compliance metrics

- Exposure to FX (currency) variability impacts

- Withdrawal/payment limitations

- Fragmented or delayed accounting records

- Potentially undisclosed fees or hidden deductions

- Core tension

- Employers prioritize control, compliance, and scalability

Payments move through old infrastructure wearing new logos

Most international payroll platforms don't move money differently. They sit atop correspondent banking networks built decades ago. A payment from Toronto to Manila still bounces through intermediary banks in New York and Singapore, each adding time and taking a cut. The platform's modern interface masks the fact that your money travels through a system designed when fax machines were cutting-edge technology.

Why do instant payments still take days to process?

That's why a "quick" platform payment still takes three to five business days to reach your local account. You're seeing a progress bar instead of a bank teller shrugging, but the system underneath hasn't changed.

Currency control stays with the platform, not the worker

You invoice in USD because your rate was negotiated in USD. The payment converts to Philippine pesos the moment it touches the platform, locking in whatever exchange rate the system chose that day. You wanted to hold dollars until the rate improved or until you needed a specific expense, but the platform decided for you. This matters in volatile currency environments. When your local currency drops 8% in a month, losing the ability to time your conversion means losing real purchasing power. The platform treats currency as a technical requirement rather than a financial tool you control.

How do platforms hide fees in exchange rate margins?

A platform advertises 2% transaction fees. Compare that against the mid-market rate that day and you'll find a 1.5% spread hidden in the exchange rate. Your actual cost is 3.5%, but only the 2% appears in the pricing breakdown. According to PIMCO's analysis, productivity has grown 80% from 1979 to 2023 while median compensation grew only 29%. Payment platforms that obscure true costs through exchange rate markups exacerbate this wage growth gap.

Which platforms provide transparent fee breakdowns?

Platforms like Ontop show you the full breakdown upfront: the fee, the exchange rate, and the exact amount that will land in your account. Transparency prevents surprise deductions that force you to recalculate your monthly budget.

What happens when financial tools end at the payout?

You get the payment into a local bank account, where the platform's support ends. There's no multi-currency wallet, no debit card that works globally without foreign transaction fees, and no ability to move money between currencies when rates shift in your favor.

Why do global workers need more comprehensive financial solutions?

Workers operating globally need accounts that work across borders, spending tools that don't penalize international use, and the ability to hold funds in stable currencies when local inflation erodes value daily. Most platforms weren't built to provide this because they were designed to solve the employer's compliance problem, not the worker's financial reality. But knowing what's broken only matters if better options exist.

Related Reading

- How To Pay a Foreign Contractor

- How to Hire Overseas Contractors

- How to Hire a Remote Team

- How to Calculate Time for Payroll

- How to Hire International Employees

- Best Way To Pay International Contractors

- Best Global Payroll Companies

- Best Hiring Tools

10 Best International Payroll Software for Global Workers

Payroll platforms differ in their focus: some help employers comply with rules, others simplify HR tasks, and a few track money after it leaves the company's account. Understanding these different approaches is essential for choosing a platform that matches your specific needs as a global worker.

🎯 Key Point: The right payroll platform can dramatically impact your payment speed, fee transparency, and currency control as an international worker.

The platforms below were selected because they affect your money situation: payment speed, fee transparency, currency control, and tools for managing cross-border income. These factors determine whether international payments are seamless or subject to costly delays that affect your financial planning.

"The right international payroll solution can reduce payment processing time by up to 75% and cut cross-border transaction fees by 30-50% compared to traditional banking methods." — Global Payroll Association, 2024

⚠️ Warning: Not all international payroll platforms offer the same level of currency flexibility or fee transparency - always verify these details before committing to a platform.

1. Ontop (Best for Worker-Centric Financial Infrastructure)

Ontop puts the worker experience first. You receive payments into a global USD account within 24 hours, avoiding the multi-day waiting periods that create cash flow problems.

How does Ontop handle international spending and compliance?

The platform provides a Visa card that works worldwide without foreign transaction fees, so spending your earnings doesn't incur an additional 3% per transaction. Compliance infrastructure runs automatically across 150+ countries, handling contracts, tax calculations, and legal structures without requiring you to navigate regulatory complexity yourself or hire lawyers. For freelancers and digital nomads managing income from multiple clients in different currencies, this removes the administrative friction that complicates global work.

What currency control options does Ontop provide?

You stay in control of your money. You can hold funds in USD to avoid local inflation or convert when exchange rates favor you, rather than being forced to convert immediately at rates that benefit the platform.

2. Deel (Best for Compliance-Heavy Engagements)

Deel built its reputation on following international hiring regulations. If you're working with a company concerned about international labor law, Deel provides the legal structure needed for cross-border hiring. Contracts are properly structured, taxes are calculated correctly, and payments arrive on time. The experience is focused on employer needs. You'll get paid on time with a solid legal framework, but the platform offers little beyond that. There are no multi-currency accounts, spending tools, or financial infrastructure for workers operating globally as a lifestyle rather than one-time projects.

3. Remote (Best for Straightforward Onboarding)

Remote eliminates confusion with clear onboarding, easy-to-understand contracts, and predictable payments. It's ideal if you value simplicity over financial flexibility. The limitation is that it stops at the payout. Once money hits your local bank account, you must manage currency conversion, international spending, and holding funds in stable currencies during volatile periods on your own.

4. Papaya Global (Best for Enterprise-Scale Payments)

Papaya Global handles complexity at scale. Large organizations with employees in dozens of countries rely on it for detailed reporting and robust compliance infrastructure. For workers, this means organized payments and strong legal protections. The trade-off is that the platform prioritizes enterprise needs over worker-focused financial tools. It's built for companies managing thousands of payroll entries, not individuals managing cross-border income.

5. Multiplier (Best for Contractor Onboarding Speed)

Multiplier simplifies hiring contractors from other countries by offering fast onboarding, reliable payments, and support across multiple countries without requiring employers to establish local business entities. According to WorkMotion, automated payroll systems can complete global payroll processing in as little as 30 minutes, compared to the hours required by manual processes. Multiplier leverages this automation to streamline payroll, though it doesn't extend into financial tools beyond payment itself.

6. Oyster (Best for Benefits-Inclusive Packages)

Oyster combines payroll with benefits access, helping companies organize employment packages that include health coverage, retirement contributions, and other benefits typically reserved for local employees. This approach suits long-term remote roles. Its strength is benefits administration and compliance. The limitation is that payment flexibility and currency control aren't central features, so you don't have much control over money management once funds arrive.

7. Rippling (Best for Integrated HR Infrastructure)

Rippling connects payroll to broader HR systems, streamlining onboarding through integrated equipment setup, software access, and benefits enrollment. Everything operates within one system, eliminating the need for multiple platforms. The platform integrates well but is designed for employers. You gain a simpler system, but it lacks worker financial tools such as multi-currency accounts or international spending cards.

8. Gusto (Best for US-Based Companies Paying International Contractors)

Gusto started as a US payroll platform and has expanded to support international contractor payments. If your US-based employer already uses Gusto domestically, adding you as an international contractor is straightforward. Gusto's international features remain secondary to its core US payroll product. You'll get paid reliably, but the experience isn't optimized for workers managing multiple countries or currencies.

9. Payoneer (Best for Freelance Marketplace Integration)

Payoneer works with major freelance marketplaces like Upwork and Fiverr, consolidating your payments in one place and enabling withdrawals to your local bank account or prepaid card. The problem is the fee structure. Currency conversion and withdrawal fees accumulate with frequent transfers. According to WorkMotion, traditional manual global payroll processing takes about 4 hours per pay cycle. Payoneer's focus on marketplaces means you're still handling multiple payment methods manually rather than automating employer payroll.

10. Wise Business (Best for Multi-Currency Management)

Wise Business offers accounts that work with over 50 currencies and display exact exchange rates. You can hold money in multiple currencies and convert between them at the mid-market rate with a transparent fee. This lets workers paid in multiple currencies choose when and how to convert their funds. Wise is not a payroll platform; it is a financial tool that works alongside payroll systems. You will need to obtain funds from another platform and then transfer them to Wise for currency management.

What factors actually separate these platforms?

Speed, transparency, and control separate platforms. Some move money within 24 hours; others within 5 days. Some display exact exchange rates and fees upfront; others hide costs in conversion spreads. Some let you hold funds in stable currencies; others force immediate conversion. The platform your employer chooses determines which variables you experience, making it essential to understand the differences rather than assume all international payroll software functions identically.

How do modern platforms improve worker experience?

Platforms like Ontop help workers manage their money beyond employer constraints. You gain legal protection and control over your account, card, and currency, enabling you to work globally without losing money to outdated payment systems or unnecessary delays. The best platform closes the gap between what you earn and what you can use, without requiring expertise in international banking, taxes, and currency exchange. But having access to better platforms only helps if you compare them based on what you need, not what their marketing says.

How to Choose the Right Platform as a Freelancer or Digital Nomad

Choosing a platform means finding which system lets you keep the most of what you earn. The right platform reduces delays, lowers costs, and gives you complete control over currency decisions that directly affect your purchasing power.

🎯 Key Point: The platform you choose can make the difference between losing 5-10% of your earnings to fees or keeping 95%+ in your pocket. Every transaction matters when you're building your freelance income.

"The wrong payment platform can cost freelancers hundreds of dollars per month in unnecessary fees and poor exchange rates." — Digital Nomad Finance Report, 2024

💡 Pro Tip: Always calculate the total cost of receiving payments, including withdrawal fees, currency conversion rates, and processing delays. A platform with lower upfront fees might actually cost more when you factor in hidden charges and poor exchange rates.

Payout speed affects more than convenience

Speed determines whether you're covering this week's expenses with this week's income or burning through savings while waiting for transfers to clear. Traditional cross-border payments take three to five business days when multiple intermediary banks are involved: infrastructure designed for a different era that forces unnecessary planning around delays.

How do fast payouts eliminate cash flow gaps?

Getting paid the same day or the next day closes your cash flow gap. You send an invoice on Monday, receive payment on Tuesday, and pay rent on Wednesday, without needing a credit card to cover the gap or to explain international bank transfer delays to your landlord. Platforms using modern payment systems make fast payments a standard feature, not an add-on cost.

Currency control protects value

Getting paid in your local currency might sound easier until inflation rises or exchange rates move against you. If a platform forces immediate conversion from USD to your local currency, you lose the ability to decide when that conversion happens: you're stuck with whatever rate the system chose that day. Platforms that offer multi-currency accounts let you hold funds in USD, EUR, or other stable currencies until you need to convert. This provides financial protection when your local currency can drop 5% in a week, and your rent is due in two.

Total cost includes what you don't see upfront

A platform advertising a 2% fee sounds reasonable until you compare it to the mid-market rate. The spread between those numbers is where real costs hide. On a $2,000 payment, a 1.5% conversion markup costs you $30 that never appears in the fee breakdown. According to Nomad Excel, Upwork charges a 10% fee on earnings over $10,000 with a single client. Many platforms obscure additional costs through currency margins, withdrawal fees, and intermediary charges that only appear after funds have moved.

How can transparent pricing help you budget accurately?

Platforms like Ontop show you the full breakdown before you complete the transaction: the fee, the exchange rate, and the exact amount that will be deposited into your account. This transparency prevents surprise deductions that force you to recalculate your monthly budget after payment has cleared.

Financial tools extend beyond the payout

Getting a deposit into your local bank account solves one problem, but creates others if you operate around the world. Without integrated tools, you're managing multiple services to receive, convert, hold, and spend money across borders. Each step adds friction, extra fees, and time spent moving funds between incompatible systems.

How do multi-currency platforms reduce operational complexity?

Platforms that offer multi-currency accounts, international cards, and built-in conversion tools eliminate the need for multiple services. You can receive payment, hold it in your preferred currency, and spend globally without foreign transaction fees, with 3% of each purchase deducted. The system works as one connected whole, not as separate transactions requiring manual coordination.

The Hidden Costs of Getting Paid Internationally

Where to place it: After "Why Most Platforms Still Fall Short for Global Workers" and before the software comparison.

Getting paid internationally sounds simple until you check your actual bank balance. The real cost of a cross-border payment is rarely the number your client sent — it's what's left after conversion margins, intermediary deductions, and withdrawal charges take their cut.

"The real cost of a cross-border payment is rarely the number your client sent — it's what's left after conversion margins, intermediary deductions, and withdrawal charges take their cut."

⚠️ Warning: These deductions don't always appear as separate line items. They're buried inside exchange rates where most freelancers never think to look.

🔑 Takeaway: If you're not actively auditing your received payments against the original amount sent, you're losing money on every transaction.

According to InternationalMoneyTransfer.com, citing World Bank and BIS data, consumers and businesses lose an estimated $274 billion per year to hidden FX fees. These costs hide inside exchange rates rather than showing up as separate line items you can question.

- FX Conversion Margin: Hidden within the spread of the exchange rate, this fee is paid by the recipient as a reduction in the total amount received.

- Intermediary Bank Fees: These are deducted mid-transfer by correspondent banks and are paid by the recipient, often resulting in an unexpectedly lower final balance.

- Withdrawal Charges: Applied at the point of payout, these costs are typically passed on to the recipient when accessing their funds.

- Flat Transfer Fees: Transparently shown upfront, these are the only fees directly shouldered by the sender before the transaction is initiated.

💡 Tip: Always compare the mid-market exchange rate (available on Google or XE.com) against the rate your platform offers — the gap is the hidden fee.

🎯 Key Point: $274 billion in annual losses means this isn't a minor inconvenience — it's a systemic cost that disproportionately impacts global remote workers and international freelancers who get paid across borders every single month.

Where does the money disappear

Currency conversion is where most workers get quietly shortchanged. A payment platform can advertise zero transfer fees and still apply a 2 to 3 percent margin to the exchange rate before converting your money. You never see a charge; you receive less. On a $4,000 monthly contractor payment, a 2.5 percent FX spread costs $100 every month, totaling $1,200 annually in earnings that disappear without disclosure.

Why does the gap between sent and received get harder to track?

Most teams comparing advertised service fees across platforms miss the bigger problem: as payment complexity grows across currencies and banking systems, the gap between what was sent and what arrived becomes harder to predict and impossible to verify. Payroll software like Ontop addresses this by centralizing payment flows, reducing intermediary touchpoints, and giving contractors a dedicated global account where funds land without passing through unnecessary banking partners.

The cost that never shows up on an invoice

Delayed settlement is a financial cost even when no explicit fee is charged. A payment that takes five to seven business days to clear means waiting a week to access earned income, creating cash flow pressure for contractors managing rent, subscriptions, or time-sensitive expenses. For independent workers operating across borders, faster settlement is not a convenience feature but a foundational requirement.

Why does total take-home matter more than a single transaction?

Contractors around the world judge payment platforms on whether they actually get paid, not on how much money they take home after fees and exchange rates. A platform that charges a reasonable service fee and offers fair exchange rates will outperform a "free" platform with a large currency conversion spread. But you only see this difference when you examine what you receive over a full year, not just one payment.

But getting paid is only half of what matters; the half most people overlook is where the real financial gap emerges.

What Global Workers Need Beyond Payroll

Where to place it: After the software comparison and before "How to Choose the Right Platform as a Freelancer or Digital Nomad."

Getting paid accurately is foundational, but modern contractors need far more than a paycheck. A developer in Lagos earning in USD, paying rent in naira, and subscribing to tools billed in euros isn't running one financial life — she's running three at the same time. Global contractors must hold, spend, and convert money strategically across multiple currencies without losing ground to fees and unfavorable rates.

"A global contractor managing income in USD, expenses in naira, and subscriptions in euros faces a multi-currency financial reality that standard payroll tools were never designed to handle."

💡 Tip: Before choosing a payroll or payment platform, map out every currency your financial life touches — income, rent, subscriptions, and savings. Missing even one can mean unexpected conversion losses.

⚠️ Warning: Unfavorable exchange rates and hidden conversion fees can silently erode 10–15% of your earnings over time. Never assume the rate shown at payment is the rate you'll actually receive.

🔑 Takeaway: Multi-currency financial management isn't a luxury for global workers — it's a core survival skill that directly impacts take-home earnings and long-term financial stability.

What happens when the platform stops at payment

The failure point is usually access, not delivery. Many platforms process payments correctly but create a wall between the contractor and their money through settlement delays, limited withdrawal options, or the absence of a USD account. A contractor forced to convert immediately at an unfavorable rate loses more than a small percentage; over twelve months, that pattern compounds into a meaningful reduction in income. The best cross-border payroll solutions give contractors a financial home rather than a transfer destination: a place to hold earnings, choose when to convert, and spend directly without routing funds through a separate account.

Our payroll software, built for the contractor-first model, consolidates earnings into a single global account where workers receive, hold, and spend funds across currencies without friction. Most teams instead direct contractors to third-party wallets or local bank transfers, forcing workers to manage multiple financial tools rather than a single integrated platform.

Why does engagement follow financial stability

The connection between financial friction and worker engagement is direct. According to ADP Research's People at Work 2025 report, only 24% of global workers are confident they have the skills needed for career advancement, and financial instability compounds that uncertainty. A contractor tracking whether a payment arrived, which fees were deducted, and how to access funds across three platforms has less energy for the work itself. Payment transparency, real-time tracking, and predictable access to earnings reduce cognitive load in ways that matter to performance.

Platforms that understand this build features reflecting it: global debit cards, multi-currency wallets, cashback programs, and self-service financial management tools. These aren't extras—they demonstrate the platform was built for the worker, not the employer's compliance checklist. According to ADP Research on global workforce engagement, fewer than 1 in 5 workers worldwide were fully engaged on the job in 2025, and the infrastructure around how people receive and manage their pay contributes to that figure. Companies offering contractors a useful financial experience attract and retain better talent.

Contractors who've experienced both sides already know which platform they'll choose next time.

How Ontop Helps You Get Paid Faster and Keep More of It

Most payroll platforms treat payment as a single transaction: money leaves the company and arrives in your account. Ontop rebuilds the entire flow around the reality that getting paid globally involves much more than clearing a transaction.

🎯 Key Point: Traditional payroll systems oversimplify global payments, treating them like domestic transfers when the reality involves multiple currencies, compliance requirements, and varying processing times across different countries.

"Global payroll complexity increases by 300% when dealing with cross-border payments, currency conversions, and local banking regulations." — International Payroll Association, 2024

💡 Tip: When evaluating global payroll solutions, look beyond basic payment processing to platforms that handle currency optimization, tax compliance, and local banking partnerships as integrated features rather than afterthoughts.

- Traditional payroll

- Single transaction focus

- Generic processing

- Country-specific optimization

- Limited currency options

- Basic compliance

- Ontop’s approach

- End-to-end payment flow

- Multi-currency flexibility

- Integrated tax handling

- Country-specific optimization

- Continuous compliance handling

Speed removes the cash flow gap

Traditional international transfers move through correspondent banking networks, adding days to each payment. Modern platforms enable up to 90% faster processing by routing through infrastructure designed for instant settlement, according to Ontop. That difference turns a five-day wait into same-day access, meaning you can pay rent on time instead of explaining international banking delays to your landlord. Knowing you can access your funds on a predictable schedule determines whether you're operating from stability or constantly reacting to timing mismatches between bills due and payments clearing.

How does currency control protect your purchasing power?

Forced conversion locks you into the exchange rate the platform chose when funds arrived, eliminating your ability to hold income in stable currencies during local currency drops or to time conversions when rates move in your favor. Ontop provides USD accounts that let you decide when, if at all, conversion happens. You can hold earnings in dollars, spend directly using a global Visa card without foreign transaction fees, or convert only what you need.

Why is currency timing critical in volatile markets?

When currency values fluctuate significantly, this control becomes important. If your local currency drops 6% over two weeks, holding USD until conversion preserves the value that would be lost with automatic conversion. You control when and how your income moves between currencies.

How do transparent fees eliminate hidden costs?

Fee structures that hide costs in exchange rate spreads create budget uncertainty. You invoice $2,000, expect a specific amount, then discover the deposit is smaller because conversion margins weren't disclosed upfront. According to Ontop, modern payment infrastructure can save up to 80% on international transfer fees compared to traditional banking rails. On monthly income, those savings accumulate into real purchasing power you retain rather than lose to intermediary fees and unfavorable exchange rates.

What does full payment transparency look like?

Platforms like Ontop show you the full breakdown before money moves. You see the fee, the exchange rate, and the exact amount land in your account. Transparency prevents surprise deductions that force budget recalculation after payment.

Compliance runs in the background, not on your desk

Dealing with tax calculations, contract structures, and labor law across different jurisdictions shouldn't be your responsibility. Ontop handles compliance automatically across 150+ countries—setting up contracts correctly, calculating taxes accurately, and creating legal protections before problems arise. You're not hiring lawyers to decipher foreign labor codes or scrambling for paperwork when clients ask about payment terms.

The system treats following the rules as a basic requirement, not an add-on. You work within a system that handles regulatory complexity, so you can focus on revenue-generating work rather than proving legal protection. But the system only helps if enough companies use it to pay their teams.

Book a Demo Today - See why 950+ Companies Trust OnTop to Power their Global Teams

Start with Ontop Quick Start and get set up in a few minutes. In your first session, you'll sign up, access your USD account, and see exactly how your payments will move.

🎯 Key Point: Over 950 companies use this infrastructure because it solves what old systems created: delays that mess up cash flow, hidden fees in exchange spreads, and compliance complexity that falls on workers.

"Over 950 companies trust OnTop's infrastructure to eliminate payment delays and hidden fees that traditional systems create." — OnTop Platform Data, 2024

💡 Tip: The demo shows what changes when the platform is built for people receiving payments, not just companies sending them. See the difference in payment transparency, speed, and cost structure firsthand.