Managing payroll across borders presents real challenges for remote workers and international teams. Juggling multiple currencies, tax regulations, and compliance requirements makes understanding outsourcing costs essential for smart financial decisions. Finding the best international payroll software can mean the difference between spending hours on administrative tasks and focusing on what actually grows a business. The true cost of outsourcing payroll includes service fees, hidden charges, time saved, and reduced compliance risks.

International payroll solutions address these challenges by streamlining payments and contractor management without requiring businesses to become tax experts or compliance specialists. The right platform handles currency conversions, local regulations, and payment processing so companies can pay their global teams accurately and on time. Whether comparing vendor pricing models or calculating return on investment for automated solutions, having proper tools transforms what seems like a complex expense into a straightforward business decision with reliable payroll software.

Summary

- Payments across borders lose an average of 6% to transaction fees, intermediary bank charges, and exchange rate margins, according to the World Bank. For someone earning $5,000 monthly, that's $300 annually lost before accounting for unfavorable conversion rates or delayed transfers. These costs don't appear on invoices or payroll dashboards, but they show up in reduced bank balances.

- International wire transfers typically take three to five business days because they pass through correspondent banking networks built before modern digital infrastructure existed. This waiting period creates real financial stress when rent or fixed expenses are due before funds clear. The unpredictability forces workers to maintain larger cash reserves than necessary, tying up capital that could be used productively.

- Automatic currency conversion strips away control over how earnings are handled. Many platforms convert income to local currency whether workers want it or not, often at rates with 2% to 4% spreads that aren't disclosed upfront. When local currencies are volatile or depreciating, workers lose the ability to hold stable currencies like USD and absorb the cost of conversion every pay cycle.

- Fee transparency remains deliberately unclear across most payment platforms. Providers distribute costs across transfer fees, intermediary charges, and FX margins without breaking down where the money goes during the transfer process. Workers see a gross amount on payslips and a smaller net deposit, with limited visibility into what happened in between.

- Most payroll systems stop at transaction completion without providing tools to manage income after it arrives. No multi-currency accounts, no integrated spending options, and no flexibility in how workers hold or use their money once deposited. The platform's responsibility ends when the transfer clears, leaving workers to navigate banking systems and currency exchanges independently.

- Payroll software addresses these challenges by offering faster transfers, transparent exchange rates, and multi-currency accounts that give workers control over when conversions happen, rather than accepting automatic decisions.

Why “Outsourcing Payroll Saves Money” Isn’t the Full Story

The efficiency argument for outsourcing payroll is accurate, but incomplete. Companies reduce administrative burden, avoid compliance penalties, and streamline operations. What receives less attention is how those same systems affect workers, particularly when money crosses borders.

🎯 Key Point: While companies see clear operational benefits from payroll outsourcing, the real impact on worker take-home pay often goes unexamined.

The moment a payment leaves one country and arrives in another, it encounters friction. Currency conversion happens. Intermediary banks take their share. Exchange rates fluctuate between when you're told you'll be paid and when the money lands in your account. These predictable outcomes reduce what workers receive.

⚠️ Warning: The gap between promised pay and actual amounts received can be significant due to these hidden costs and delays in cross-border transactions.

"Cross-border payment friction creates a hidden tax on international workers that companies rarely factor into their total compensation calculations." — Global Payroll Analysis, 2024

What are the typical fees for cross-border payments?

According to the World Bank, the global average cost of sending money across borders is around 6%, with some corridors charging significantly more. This includes transfer fees, intermediary bank charges, and exchange rate margins often undisclosed upfront. For someone earning $5,000 monthly, that's $300 in transaction costs alone, before accounting for unfavorable exchange rates or delayed transfers.

How do transfer delays impact cash flow?

International wire transfers often take three to five business days, creating financial stress for those who need consistent cash flow for rent, utilities, or other regular expenses. Automated currency conversion adds uncertainty: you might agree to an exchange rate on Monday, but if the transfer processes on Thursday and markets shift, the amount you receive reflects Thursday's rate rather than the expected one.

How do payment delays affect workers' daily lives?

The gap between what a company pays and what a worker receives shows up in bank statements, in the difference between gross and net deposits, and in the frustration of explaining to a landlord why rent will be two days late. According to the National Small Business Association, 40% of small business owners spend over 80 hours per year on payroll tasks, while workers spend their own time fixing mistakes, contacting support teams, and managing delayed or reduced payments.

Why do workers lose control over their money transfers?

When your earnings are automatically converted and transferred through systems you didn't choose, you lose control over how your money is handled. You cannot select a better exchange rate, time the transfer to avoid market dips, or access cheaper alternatives. You accept whatever process the payroll provider uses.

Related Reading

- Best International Payroll Software

- Pay International Employees

- How Much Does It Cost To Outsource Payroll

- Global Payroll Implementation

- Benefits Of Hiring Remote Workers

- International Payroll Management

- Multi-Country Payroll Outsourcing

What “Outsourced Payroll” Actually Means for Workers

Outsourced payroll determines the infrastructure through which your income flows. It shapes payment speed, transaction costs, legal classification, and the reliability of every deposit you depend on. When a company hands payroll to a third party, they cede control of how, when, and through what channels you get paid.

🎯 Key Point: Your payment experience is no longer controlled by your direct employer but by their chosen payroll provider.

"When companies outsource payroll, they transfer operational control of worker payments to external providers, fundamentally changing the employee payment experience." — Payroll Management Research, 2024

⚠️ Warning: Third-party payroll systems can introduce unexpected delays, additional fees, or technical issues that your employer may have limited ability to resolve quickly.

How payment methods shape your access to money

Digital wallets, wire transfers, and specialized payment systems have different processing times and fees. Some lock you into specific banks or require additional accounts. Others add steps that delay access to earned money. According to Pentabell, 40% of businesses outsource their payroll functions, meaning millions of workers use payment systems they didn't choose and can't easily change. A direct bank transfer might take three days. A digital wallet could arrive in hours, but charge withdrawal fees. The company optimizes for operational efficiency, while you bear the consequences in the form of longer wait times and lower take-home pay.

What processing layers slow down your payments?

Multiple compliance checks, banking intermediaries, and currency conversion steps create delays between payroll approval and money landing in your account. A payment might clear the payroll system on Tuesday but not reach your bank until Friday after passing through correspondent banks in two countries. Timing isn't guaranteed; it depends on typical processing windows, making financial planning unpredictable.

How does outsourced payroll efficiency affect payment timing?

PrimePay Blog reports that outsourced payroll processing takes about 30 minutes compared to 4 hours for in-house processing. However, this speed improvement benefits the employer. For workers, what matters is the time between "payment sent" and "funds available"—a window that doesn't necessarily shorten because the company's paperwork burden did.

Legal classification and contract structure

How your job is categorized affects tax withholding, benefit eligibility, and legal protections. Outsourced payroll systems often standardize contract types to simplify processing, which can misclassify workers or strip protections available under different arrangements.

What happens when payroll systems misclassify workers?

Incorrect structuring may create unexpected tax liabilities months later, even when payments arrive on time. Workers at Howard Community College experienced this directly: incorrect federal tax withholdings and delayed retirement contributions created financial uncertainty that payroll dashboards failed to flag. The system processed payments efficiently from the employer's perspective while extracting money from workers' pockets through recurring errors across pay periods. Understanding how outsourced payroll works reveals only half the picture; the other half is knowing where your money goes before it reaches you.

The Real Cost Breakdown (From a Worker’s Perspective)

The listed fee isn't the real problem. Transaction fees, currency conversion spreads, payment delays, and compliance gaps reduce what you receive. These hidden costs don't appear on invoices or dashboards, but they show up in your bank balance.

🎯 Key Point: The advertised rate is just the starting point - multiple layers of fees and delays eat into your actual earnings before the money hits your account.

"Hidden fees and conversion spreads can reduce freelancer earnings by 15-25% beyond the platform's stated commission." — Freelancer Economics Report, 2024

⚠️ Warning: Most workers only calculate the platform fee when budgeting projects, completely missing the additional costs that can significantly impact their actual take-home pay.

Transaction fees across payment corridors

Every cross-border payment passes through intermediaries, each taking a percentage. According to the World Bank (2024), the global average cost of sending money across borders is 6%, with some routes charging significantly more. A $4,000 monthly salary loses $240 annually to transaction costs alone. The route matters. Payments between certain countries go through more intermediary banks, each adding its own processing fee. You don't choose the route; the payroll system does, and you pay whatever cost structure results.

Currency conversion spreads

Banks and payment providers add extra charges on top of market exchange rates. A 2% to 4% spread seems small until you calculate it across a regular income. If you earn $5,000 monthly and conversion happens at a 3% margin, you lose $150 every month—$1,800 annually—to exchange rate markups you never agreed to. The quoted rate at approval often differs from the rate applied when the transfer processes. Platforms like payroll software address this by offering clear FX rates and reducing conversion layers, which cuts the gap between what's sent and what arrives.

How do payment delays affect your cash flow?

International transfers take three to five business days, sometimes longer. This delay complicates fixed expenses: rent due on the first won't wait for a payment clearing on the third. Late fees, overdraft charges, and missed bill payments create extra costs stemming directly from processing delays beyond your control.

Why does timing uncertainty create additional costs

Timing uncertainty worsens the problem. You might expect payment on Tuesday, but compliance checks or intermediary bank processing delay it to Thursday. This unpredictability forces you to maintain larger cash reserves than necessary, capital you cannot invest, save, or use productively. But even when payments arrive on time, another layer of cost often surfaces months later: one that's harder to spot and more expensive to fix.

Related Reading

- How To Pay a Foreign Contractor

- How to Hire Overseas Contractors

- Benefits Of Hiring Remote Workers

- International Payroll Management

- Best Way To Pay International Contractors

- Benefits Of Hiring International Employees

- Best International Payroll Providers

- B2b Cross-border Payments

Why Most Payroll Providers Still Create Friction

More payroll providers should mean better options for workers. Instead, most platforms copy the same structural problems: they're built to move money efficiently from company to worker, but not to optimize what happens after payment leaves the company's account. They treat payment completion as the finish line when, for you, it's the starting point of managing your income.

🎯 Key Point: Traditional payroll systems focus on employer efficiency, not worker financial outcomes after payment delivery.

"Payment completion is treated as the finish line when, for workers, it's just the starting point of managing income."

⚠️ Warning: This fundamental misalignment means most payroll platforms optimize for the wrong end user—leaving workers to navigate income management alone.

Payments still move through outdated banking rails

Cross-border transfers rely on correspondent banking networks designed decades before digital payments existed. Your salary passes through multiple intermediaries, each adding compliance checks, settlement delays, and processing fees. According to PayPro, average payroll processing time with legacy systems runs 3 to 5 days. Providers favor familiar banking partnerships over faster alternatives because integration is easier and cheaper for them, not due to technical limitations. The route your payment takes is optimized for the provider's operational simplicity, not for speed or cost. You wait longer and pay more as a result.

Currency control gets stripped away

Many platforms automatically convert your earnings into local currency without asking you first, removing your ability to hold stable currencies like USD when your local currency fluctuates significantly. Conversion rates are not shared with you: typically, 2% to 4% margins are hidden behind "competitive FX rates" marketing claims. Platforms like payroll software give workers control over currency decisions and transparent conversion rates. With Ontop, you gain visibility into exactly how much you're receiving in your chosen currency, reducing the gap between what's sent and what arrives. These compounds monthly across each pay cycle.

Fee transparency remains deliberately unclear

The World Bank reports that global cross-border payment costs average around 6%, distributed across transfer fees, intermediary bank charges, and FX margins. Providers rarely explain where the money goes during the transfer process. Workers see a gross amount on their payslip and a smaller net deposit in their account, with limited visibility into what happens in between. Clearer fee structures would force providers to justify costs that workers might reject if they understood them fully.

What happens when platforms stop at transaction completion?

Most payroll systems don't provide tools to manage your money after it arrives: no USD accounts, spending options, or choices for how you keep or use your funds once deposited. The platform stops working once the transfer completes, leaving you to navigate banking systems, currency exchanges, and cash management independently. You get $1,000, wait several days for it to show up, lose some to fees and conversion, then figure out how to protect what remains from further loss in value.

Why do payroll systems prioritize transactions over worker experience?

The system is designed to complete a transaction, not to help you get the best financial outcome. Until providers treat worker experience as equally important as employer convenience, getting paid globally will remain slower, less transparent, and more expensive than it should be. Knowing the problems only gets you halfway. The harder question is figuring out which solutions fix them.

How to Evaluate Payroll Solutions as a Worker

Most advice focuses on features. What matters is how the system affects your money in practice. Payout speed and reliability should be your primary evaluation criteria, not flashy interfaces or marketing promises.

Start with payout speed and reliability. Delays are systemic: according to the Bank for International Settlements, international payments often involve multiple correspondent banks, which increases settlement time and uncertainty. Some transfers still take days instead of hours.

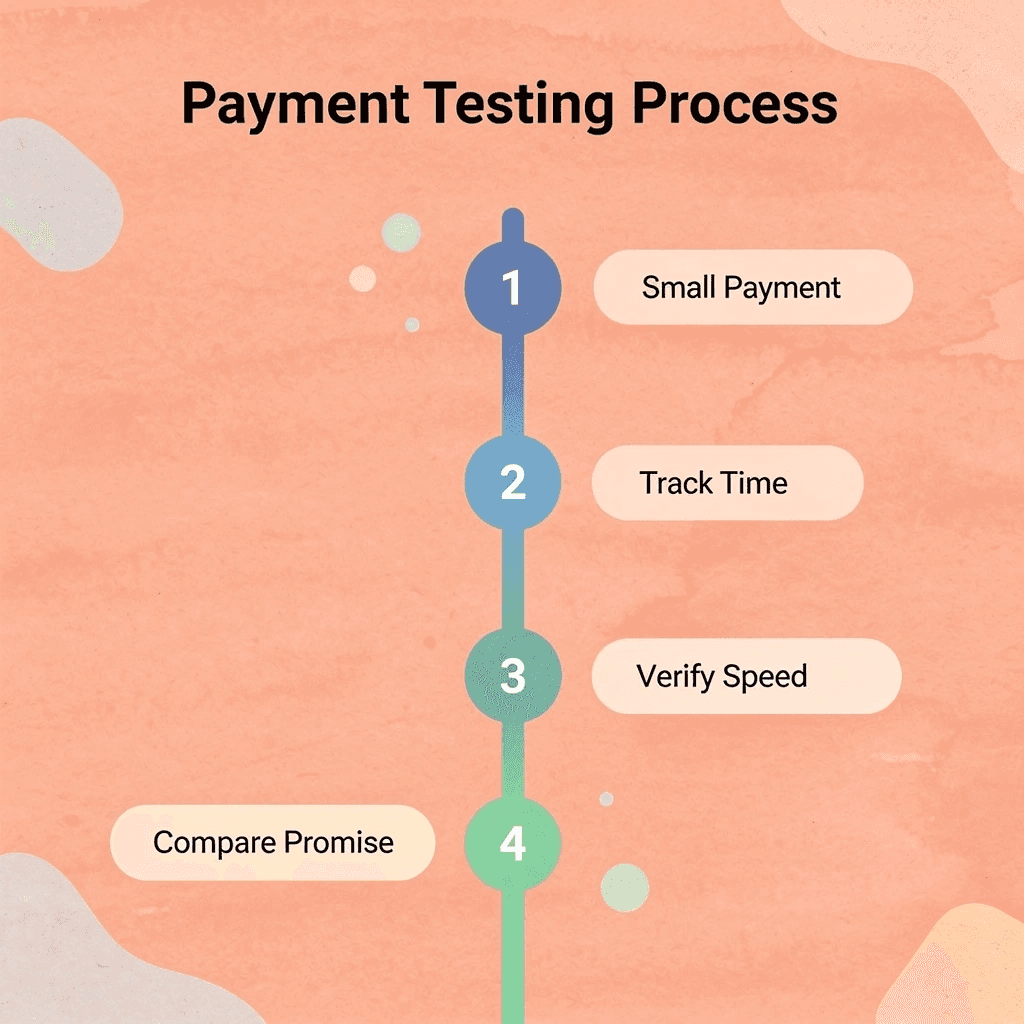

💡 Pro Tip: Test the payroll system with a small payment first to verify actual processing times versus promised delivery windows.

"International payments often involve multiple correspondent banks, which increases settlement time and uncertainty." — Bank for International Settlements

🔑 Key Takeaway: Don't just read the fine print—experience the payment flow yourself before committing to any payroll solution for your regular income.

The true cost of getting paid

Look at the real cost, especially foreign exchange margins. Many providers claim low or zero transfer fees but still profit from exchange rate fluctuations. According to OECD, exchange rate markups can constitute a significant portion of total transfer costs, sometimes exceeding the advertised fee. Focus on the net amount you receive, not the advertised fee. Access to stable currencies like USD is important. In many countries, currency fluctuations directly affect purchasing power. Data from the International Monetary Fund show that emerging market currencies can shift significantly in the short term, reducing their value if conversion occurs automatically.

How should compliance be built into the platform?

Compliance should be built into the platform to ensure predictability. Different regulatory rules across countries create problems in cross-border work. A good system handles this in the background, protecting you from gaps.

What financial infrastructure features matter most?

Most platforms stop after the transaction is complete, leaving you to manage currency exposure, banking access, and cash flow independently. Solutions like payroll software address this by offering multi-currency accounts and transparent FX rates, reducing the need for additional services and extra fees. The difference is how things work: faster access, clearer costs, and control over your earnings, rather than slow transfers and disconnected tools. Better infrastructure improves the efficiency with which you earn, receive, and use money.

How Ontop Helps You Keep More and Get Paid Faster

Most payroll systems move money from employer to worker and consider the job done. Ontop operates differently by treating the worker's financial outcome—how much you keep, how quickly you access it, and how easily you use it—as the main metric, not simply completing the transaction.

🎯 Key Point: Traditional payroll focuses on transaction completion, while Ontop prioritizes your financial success and money accessibility.

"Ontop operates differently by treating the worker's financial outcome as the main metric, not just completing the transaction."

💡 Tip: Look for payroll solutions that optimize for your financial needs—faster access, lower fees, and easier money management—rather than just moving money from point A to point B.

Speed matters more than most platforms admit

Cross-border payments traditionally take three to five business days through correspondent banking networks built before modern infrastructure existed. Bamboo Payment Systems reports that Ontop enables real-time payouts, eliminating the waiting period that forces workers to maintain larger cash reserves or miss payment deadlines. Faster processing improves cash flow management and reduces secondary costs such as late fees and overdraft charges.

Currency control changes what you keep

Automatic conversion at provider-set rates removes your ability to protect earnings from currency fluctuations or unfavorable exchange rates. Ontop provides USD accounts, letting you hold income in a stable currency and decide when conversion makes sense rather than accepting whatever rate applies at transfer time. According to Ontop, this approach can save up to 80% on international transfer fees compared to traditional banking routes. This difference compounds across every pay cycle, particularly in markets where local currency fluctuates significantly.

What makes payment systems truly usable?

Getting paid is one thing. Being able to spend or withdraw it without extra steps, fees, or switching between platforms is another. A global Visa card built into Ontop's payment system makes your earnings immediately usable without moving funds to outside accounts or managing currency exchange separately. Compliance is handled within the same system, reducing classification risk and tax uncertainty.

How does integrated infrastructure change financial outcomes?

Instead of waiting days for a transfer, losing money to hidden exchange rate fees, and figuring out how to access what remains, you receive funds faster, control when conversion happens, and use your income directly through integrated tools. That is not a feature list. That is a different financial outcome. But knowing what better infrastructure looks like matters only if you can access it.

Related Reading

- Best Payroll Software For Staffing Companies

- Best Payroll Outsourcing Companies

- Deel Vs Oyster

- Best International Payroll Software

- Best Payroll For Contractors

- Remote Competitors

- Velocity Global Competitor

- ADP Alternative

Book a Demo Today - See why 950+ Companies Trust OnTop to Power their Global Teams

Ontop Quick Start gets you set up in minutes. In your first session, you'll see exactly how payments flow to you, how much you keep after fees and conversion, and how quickly funds become available to spend or withdraw.

💡 Tip: Experience the difference in your first demo session - see real payment flows, transparent fees, and actual transfer speeds side by side.

"Over 950 companies use Ontop because the math works differently - faster transfers improve cash flow and transparent FX rates keep more money in your account." — OnTop Client Success Data, 2024

Over 950 companies use Ontop because the math works differently. Faster transfers improve cash flow. Transparent FX rates keep more money in your account. USD holding accounts let you control when conversion happens instead of accepting automatic conversions that reduce earnings. These measurable differences appear in every payroll cycle.

Traditional Payment Systems

OnTop Advantage

Slower transfers

Faster payment processing

Hidden fees

Transparent FX rates

Automatic conversions

USD holding accounts with conversion control

Reduced earnings

More money stays in your account

🎯 Key Decision Point: The question is whether you'll keep accepting slower transfers, hidden fees, and automatic conversions, or spend fifteen minutes seeing what changes when the system is built around your outcome instead of just transaction completion.

The question is whether you'll keep accepting slower transfers, hidden fees, and automatic conversions, or spend fifteen minutes seeing what changes when the system is built around your outcome instead of transaction completion.